You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Pakistan economy related news

- Thread starter Zeeman

- Start date

Pakistan Space Agency

NEW RECRUIT

IMF – Back to square 1

February 6, 2022

By Khurram Husain

In the last full year of its term, the PTI government has managed to land itself back to the same position it was in at the beginning, back in 2018. Once again they are looking at a severe adjustment to control a ballooning current account deficit, a raft of deeply popular tax measures to shore up the fiscal equation and continued hikes in interest rates to curb inflation. In short, once again they have to apply the brakes to growth in order to manage growing macroeconomic instability, and along the way pay the political price that comes with such measures.

Look at the projections for the current account deficit (CAD) in the remaining months of the fiscal year, running from January to June 2022. In line with the State Bank’s projection, the CAD is expected to reach $13 billion by June 2022 according to the IMF. At the same time, gross official reserves stock is expected to hit $21.2bn, when it currently stands at $17.7 (including the one billion dollar each from the IMF tranche and the recent Sukkuk flotation).

Now consider this. The CAD has already reached $9bn in the July to December period, meaning it can only rise by another $4bn at best in the remaining months of the fiscal year to remain within the program projection. This means an average monthly CAD of $666 million for the next six months where it has averaged $1.5bn per month so far. How is such a sharp deceleration in the CAD to be achieved?

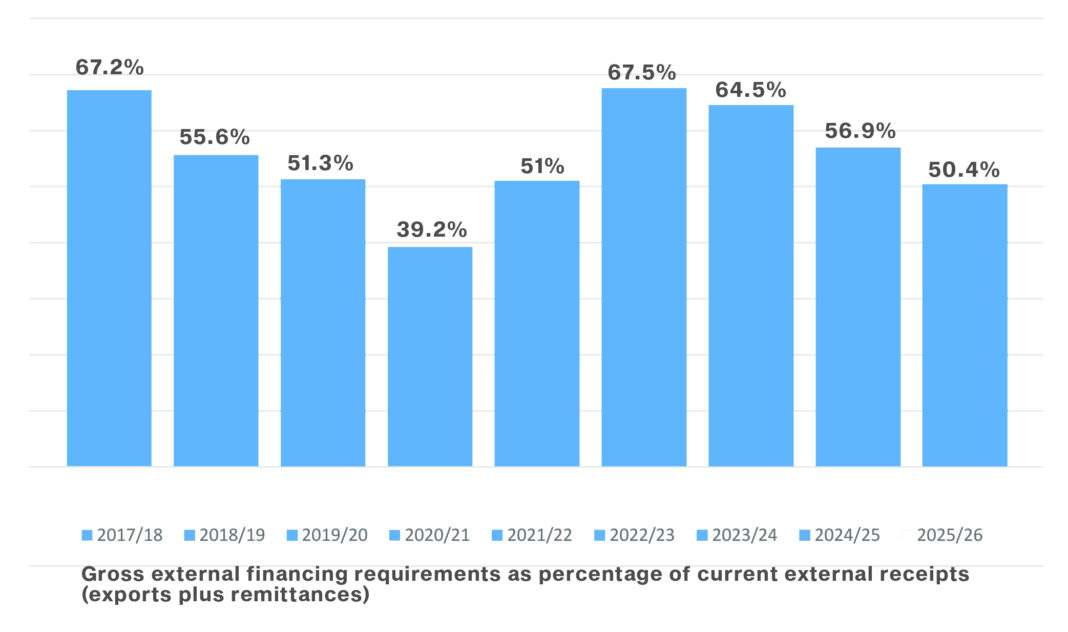

The only way would be through a sharp deceleration in the trade deficit. But the program projects anything but a deceleration. According to the original projection on trade deficit (goods, services and net income) for FY2022 made back last April this deficit was supposed to come in at $34bn by this June. In the projection made in the latest document released on Friday, this amount will be more than $45bn. For the next few years it is projected to remain around this level, meaning the additional import requirement that the economy has added since April last year now has to be carried through more stringent reserve accumulation measures. Perhaps this partly explains the sharp jump in the external financing needs, the near unseemly urgency of the government to borrow (lifting a billion dollars from international markets at exorbitantly high interest rates even before the IMF program had been approved by the board).

The government’s stint in power began with the country facing a massive current account deficit and a troubled approach to the IMF for immediate assistance. It took them nine months to get an agreement on a Fund program, and jettison their star finance minister – Asad Umar – along the way. From November 2018, when the negotiations began, till July 2019, when they were concluded with Hafeez Shaikh’s signature, the government cut a difficult path trying to water down the scale of the adjustment the fund was demanding and soften some of the conditions. Nine months later they signed on the dotted line, after removing their finance minister and bringing another one in.

profit.pakistantoday.com.pk

profit.pakistantoday.com.pk

February 6, 2022

By Khurram Husain

In the last full year of its term, the PTI government has managed to land itself back to the same position it was in at the beginning, back in 2018. Once again they are looking at a severe adjustment to control a ballooning current account deficit, a raft of deeply popular tax measures to shore up the fiscal equation and continued hikes in interest rates to curb inflation. In short, once again they have to apply the brakes to growth in order to manage growing macroeconomic instability, and along the way pay the political price that comes with such measures.

Look at the projections for the current account deficit (CAD) in the remaining months of the fiscal year, running from January to June 2022. In line with the State Bank’s projection, the CAD is expected to reach $13 billion by June 2022 according to the IMF. At the same time, gross official reserves stock is expected to hit $21.2bn, when it currently stands at $17.7 (including the one billion dollar each from the IMF tranche and the recent Sukkuk flotation).

Now consider this. The CAD has already reached $9bn in the July to December period, meaning it can only rise by another $4bn at best in the remaining months of the fiscal year to remain within the program projection. This means an average monthly CAD of $666 million for the next six months where it has averaged $1.5bn per month so far. How is such a sharp deceleration in the CAD to be achieved?

The only way would be through a sharp deceleration in the trade deficit. But the program projects anything but a deceleration. According to the original projection on trade deficit (goods, services and net income) for FY2022 made back last April this deficit was supposed to come in at $34bn by this June. In the projection made in the latest document released on Friday, this amount will be more than $45bn. For the next few years it is projected to remain around this level, meaning the additional import requirement that the economy has added since April last year now has to be carried through more stringent reserve accumulation measures. Perhaps this partly explains the sharp jump in the external financing needs, the near unseemly urgency of the government to borrow (lifting a billion dollars from international markets at exorbitantly high interest rates even before the IMF program had been approved by the board).

The government’s stint in power began with the country facing a massive current account deficit and a troubled approach to the IMF for immediate assistance. It took them nine months to get an agreement on a Fund program, and jettison their star finance minister – Asad Umar – along the way. From November 2018, when the negotiations began, till July 2019, when they were concluded with Hafeez Shaikh’s signature, the government cut a difficult path trying to water down the scale of the adjustment the fund was demanding and soften some of the conditions. Nine months later they signed on the dotted line, after removing their finance minister and bringing another one in.

IMF – Back to square 1

More rate hikes, currency depreciation, taxes, expenditure restraints are now on the cards as the government finally moves to unwind its stimulus measures and return to stabilization with the resumpti